- Net Income Declined 7.3 Percent from Third Quarter 2018 Due to Nonrecurring Events at Three Large Institutions

- Net Interest Margin Declined from a Year Ago to 3.35 Percent

- Community Bank Quarterly Earnings Increased 7.2 Percent Year Over Year

- Total Loan and Lease Balances Increased from the Previous Quarter and a Year Ago

- The Number of Banks on the “Problem Bank List” Remained Low

Despite nonrecurring events at three large institutions that impacted overall net income, the banking industry reported positive results this quarter. With the sustained economic expansion, the FDIC urges banks to uphold careful underwriting standards and prudent risk management.” — FDIC Chairman Jelena McWilliams

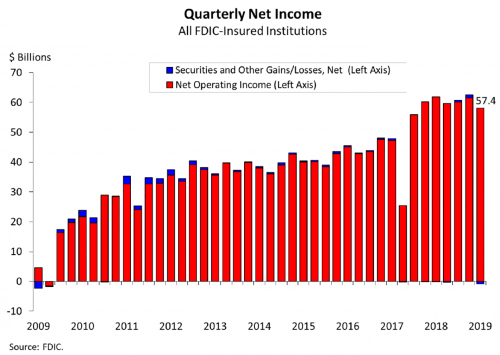

For the 5,256 commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC), aggregate net income totaled $57.4 billion in third quarter 2019, a decline of $4.5 billion (7.3 percent) from a year ago. The decline in net income was caused by higher noninterest expense and loan-loss provisions and realized securities losses. Financial results for third quarter 2019 are included in the FDIC’s latest Quarterly Banking Profile released last week.

“The banking industry reported positive results this quarter, despite nonrecurring events at three large institutions that affected quarterly net income,” McWilliams said. “Overall, the banking industry reported strong loan growth, and the number of ‘problem banks’ remained low. Community banks also reported another positive quarter. Net income at community banks improved due to higher net operating revenue, and the annual rate of loan growth at community banks exceeded the overall industry.”

“This quarter, we also saw two reductions in short-term interest rates and a flat yield curve, which present new challenges in credit extension and funding. It is imperative that banks maintain careful underwriting standards and prudent risk management in order to maintain lending through this economic fluctuation.”

Highlights from the Third Quarter 2019 Quarterly Banking Profile

Net Income Declined 7.3 Percent from Third Quarter 2018 Due to Nonrecurring Events at Three Large Institutions: The 5,256 FDIC-insured institutions reported aggregate net income of $57.4 billion in third quarter 2019, a decline of $4.5 billion (7.3 percent) from a year ago. The quarterly decline in net income was due to nonrecurring events at three large institutions. However, 62 percent of all institutions reported a year-over-year increase in net income; slightly more than 4 percent of institutions were unprofitable. The average return on assets declined from 1.41 percent in third quarter 2018 to 1.25 percent.

Community Banks’ Net Income Increased 7.2 Percent from Third Quarter 2018: The 4,825 FDIC-insured community banks reported net income of $6.9 billion in third quarter 2019, up $466 million from a year ago. Pretax return on assets rose 3 basis points to 1.51 percent, marking the highest quarterly pretax return on assets reported by community banks since third quarter 2006. Growth in net interest income (up 4 percent to $19 billion), noninterest income (up 16.4 percent to $5.1 billion), and gains on securities sales (up 675.1 percent to $164.5 million) were responsible for the annual increase in profitability. Revenue growth in these areas offset increases in noninterest expense (up 5.8 percent to $15.2 billion), provision expense (up 24.9 percent to $754 million), and income tax expense (up 12 percent to $1.4 billion).

Net Interest Income Increased 1.2 Percent from a Year Ago: Net interest income increased by $1.7 billion (1.2 percent) from 12 months ago, making it the lowest annual growth rate since fourth quarter 2014. Lower yield on earning assets contributed to the slowdown in net interest income. However, slightly more than two-thirds of all banks (70.9 percent) reported annual increases in net interest income. The average net interest margin declined by 10 basis points from a year ago to 3.35 percent.

Total Loan and Lease Balances Increased from the Previous Quarter and a Year Ago: Total loan and lease balances increased by $99.5 billion (1 percent) from the previous quarter. Growth among major loan categories was led by consumer loans, which includes credit cards (up $31.3 billion, or 1.8 percent) and residential mortgage loans (up $22 billion, or 1 percent). Over the past year, total loan and lease balances rose by 4.6 percent, slightly above the 4.5 percent annual growth rate reported last quarter. Commercial and industrial loans registered the largest dollar increase from a year ago (up $131.9 billion, or 6.3 percent).

Asset Quality Indicators Remained Stable: The amount of loans that were noncurrent (i.e., 90 days or more past due or in nonaccrual status) declined by $184.8 million (0.2 percent) from the previous quarter. Noncurrent balances reported mixed results for major loan categories. Residential mortgages declined by $407.4 million (1 percent), while credit card balances rose by $940.9 million (8.1 percent) and commercial and industrial loans increased by $263.5 million (1.5 percent). The average noncurrent loan rate declined by 1 basis point from the previous quarter to 0.92 percent. Net charge-offs rose by $1.9 billion (17.2 percent) from a year ago, and the average net charge-off rate rose to 0.51 percent.

The Number of Banks on the “Problem Bank List” Remained Low: The number of problem banks fell from 56 to 55 during the third quarter, the lowest number of problem banks since first quarter 2007. Total assets of problem banks rose modestly from $48.5 billion in the second quarter to $48.8 billion.

The Deposit Insurance Fund’s Reserve Ratio Rose to 1.41 Percent: The Deposit Insurance Fund (DIF) balance totaled $108.9 billion in the third quarter, an increase of $1.5 billion from the previous quarter. The quarterly increase was due to assessment income, interest earned on investment securities held by the DIF, and a reduction in losses from past failures. The reserve ratio rose by 1 basis point from the previous quarter to 1.41 percent.

Mergers and New Bank Openings Continued in the Third Quarter: During the third quarter, four new banks opened, 46 institutions were absorbed by mergers, and no banks failed.

Chattooga Local News

Federal Correctional Officer Convicted of Bribery, Smuggling, and Drug Conspiracy

Chattooga Local Government

Reps. Davis, Scott and Schofield: We Oppose House Bill 297

Chattooga Local News

Carr Launches “Eyes on the Road” Campaign to Locate Georgia’s Missing Children

Bulloch Public Safety

04/06/2026 Booking Report for Bulloch County

Chattooga Schools

Kindergarten Registration Opens April 15 in Chattooga County

Bulloch Public Safety

03/09/2026 Booking Report for Bulloch County

Bulloch Public Safety

03/30/2026 Booking Report for Bulloch County

Bulloch Public Safety

03/16/2026 Booking Report for Bulloch County

Bulloch Public Safety

03/10/2026 Booking Report for Bulloch County

Bulloch Public Safety

03/20/2026 Booking Report for Bulloch County